"Quack Attack" Soars in Vanguard ETF Trading Competition

When the opportunity to enter the Vanguard ETF Trading Competition arose, a group of second-year Stevens School of Business quantitative finance majors answered the bell. After finishing near the top of the leaderboard, they experienced an iconic one ringing.

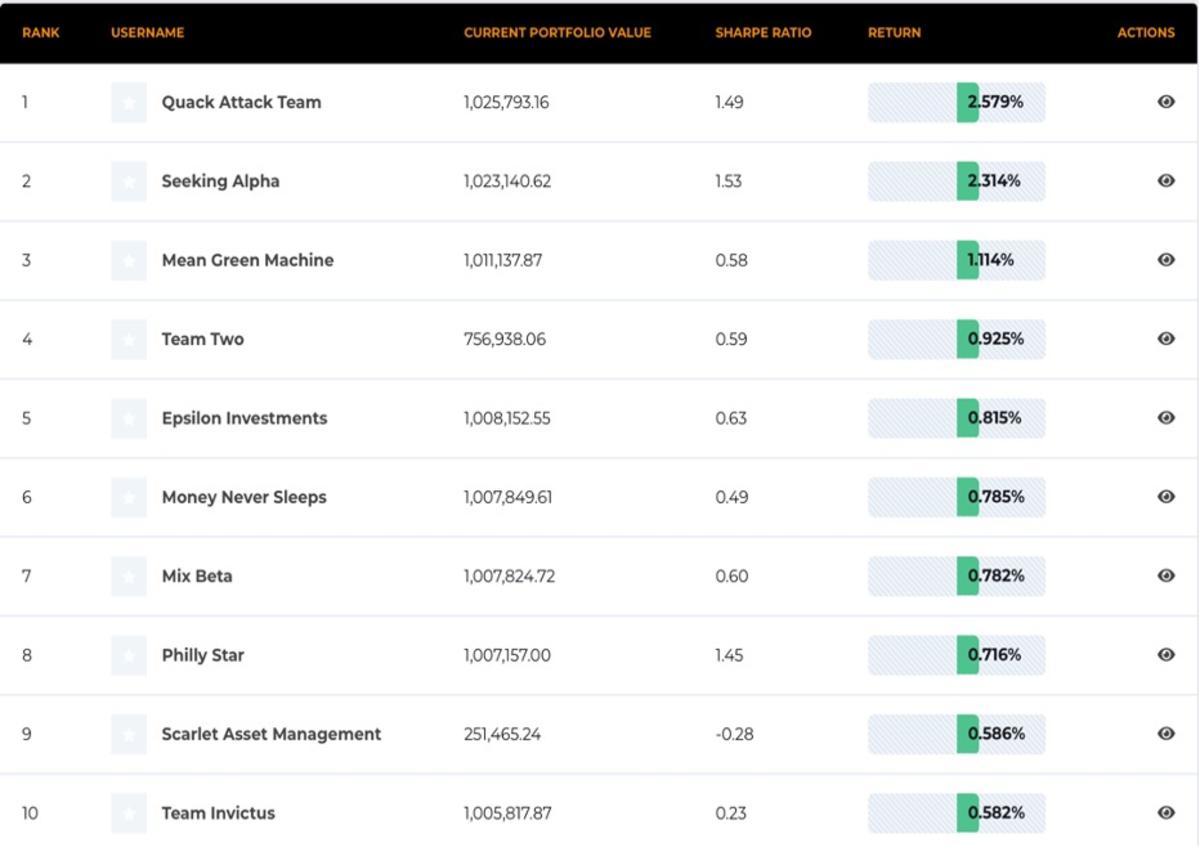

The Vanguard ETF Trading Competition is an annual eight-week investing challenge in which student teams actively manage a simulated portfolio composed entirely of Vanguard ETFs. Performance is ranked by the Sharpe ratio, so teams focus on generating strong returns while keeping volatility low. Throughout the competition, teams track portfolio value, return and Sharpe ratio in real time.

Connor Byhre (Chicago), Mathew Ginzburg (Brooklyn), Gabriel Malek (North Caldwell, NJ), Vikram Vegiraju (Morganville, NJ) and Armaan Seth (Princeton, NJ) — known to the other competitors as the “Quack Attack” — finished first in total return at 2.58%, making them the only team to outperform the S&P 500. The quintet placed second overall with a Sharpe ratio of 1.49, almost twice that of the S&P 500 in the same period.

As finalists, the group was invited to pitch a custom exchange-traded fund concept to Vanguard and visited the New York Stock Exchange for the closing bell.

“The most rewarding part was being invited to the New York Stock Exchange as finalists,” Vikram said. “Being on the floor for the closing bell was an incredible experience, and meeting Peter Tuchman, the 'Einstein of Wall Street,’ made it even more memorable.”

The team built its success on the foundation of staying focused on the data. They gathered the entire price history of every Vanguard ETF, broke it into eight-week segments to match the competition’s format and then ran millions of simulated portfolios under the same rules.

The team built its success on the foundation of staying focused on the data. They gathered the entire price history of every Vanguard ETF, broke it into eight-week segments to match the competition’s format and then ran millions of simulated portfolios under the same rules.

“Our strategy was entirely data driven,” Connor said. “To prevent overfitting, we used a variation of the Sharpe ratio that puts more of a penalty on volatility, because that is far more predictable than returns. After validating the results on test data, we applied the weights in the live competition and only made small adjustments around major economic reports to avoid volatility spikes.”

The team divided the workload to maximize their strengths and efficiency. Connor built the quantitative framework, creating the simulation that powered the team’s risk-adjusted portfolio decisions. Matthew added a complementary angle by analyzing win rates instead of relying solely on expected performance, helping the group guard against early setbacks. Gabriel monitored major economic reports and guided the timing of position changes around potentially volatile events, while Vikram kept a close eye on the leaderboard and tracked competitors for possible hedging opportunities or strategic insights. Armaan, while not officially on the team’s roster, served as an advisor, offering input on key investment decisions throughout the competition.

“Probability, Statistics, and Stochastic Processes, taught by Professors Thomas Lonon, Anthony Diaco and Sveinn Olafsson, were the classes that best prepared us for the trading challenge,” Armaan said. “Their courses gave us the tools for expectations, correlation, random walks and statistical testing that we relied on when building and validating our strategy.”

For their pitch, the team created RHO, an ETF that doesn’t tie investors to the S&P 500's overall performance. Inside their fund was a mix of different investment types that don’t move in the same direction under similar conditions. The two-layer approach was designed to give investors a single, easy investment option with less volatility and strong long-term performance.

“The idea had two layers,” Matthew explained. “First, low correlation to the S&P 500 and second, diversifying within the ETF by combining assets and sectors that have low correlations to each other. We used millions of efficient-frontier simulations to build a mix that stayed stable across different market environments. It ended up being a genuinely enjoyable and creative project, and presenting it to Vanguard was one of the highlights of the entire competition.

The team believes its focus on the competition rules and data enabled them to succeed. By making decisions that fit the challenge's structure rather than trying to outguess the market, they were able to stay consistent throughout the eight weeks. The team’s recipe for success is something they think future Stevens’ competitors can emulate.

“Our biggest advice is to keep things simple and follow a clear process,” Gabriel said. “The market is usually priced efficiently, so don’t assume you can outsmart it. Instead, understand the structure of the competition and build your approach around those rules. Traditional strategies don’t always work over an eight-week window, so focus on what the competition gives you, like the ability to see other teams’ positions before major economic events. It also helps to use campus resources such as Capital IQ or Bloomberg to support your research and test your ideas.”

“Our biggest advice is to keep things simple and follow a clear process,” Gabriel said. “The market is usually priced efficiently, so don’t assume you can outsmart it. Instead, understand the structure of the competition and build your approach around those rules. Traditional strategies don’t always work over an eight-week window, so focus on what the competition gives you, like the ability to see other teams’ positions before major economic events. It also helps to use campus resources such as Capital IQ or Bloomberg to support your research and test your ideas.”