Stevens School of Business Ph.D. researcher, Agathe Sadeghi, explores innovative method to uncover causal relationships in financial data

When you walk into a dark room, turn on a switch and light appears, or you turn the key in a car’s ignition and it starts, you’re experiencing cause and effect in action. It’s an action causing a change that affects something else.

It’s also important to note that causation shouldn’t be mistaken for correlation. Say it’s a hot day, and you’re eating ice cream and realize you forgot to wear sunscreen. As your ice cream melts, you also see your arms getting red simultaneously. While the two are correlated, melting ice cream isn’t causing you to get a sunburn or vice versa. Instead, the sun is responsible for both events and creating the correlation. This makes causal discovery complex.

It’s also important to note that causation shouldn’t be mistaken for correlation. Say it’s a hot day, and you’re eating ice cream and realize you forgot to wear sunscreen. As your ice cream melts, you also see your arms getting red simultaneously. While the two are correlated, melting ice cream isn’t causing you to get a sunburn or vice versa. Instead, the sun is responsible for both events and creating the correlation. This makes causal discovery complex.

While we may understand and can easily predict these everyday examples, when trying to predict how certain factors may impact stock prices to develop a solid trading strategy, things get a lot less clear and more challenging to determine.

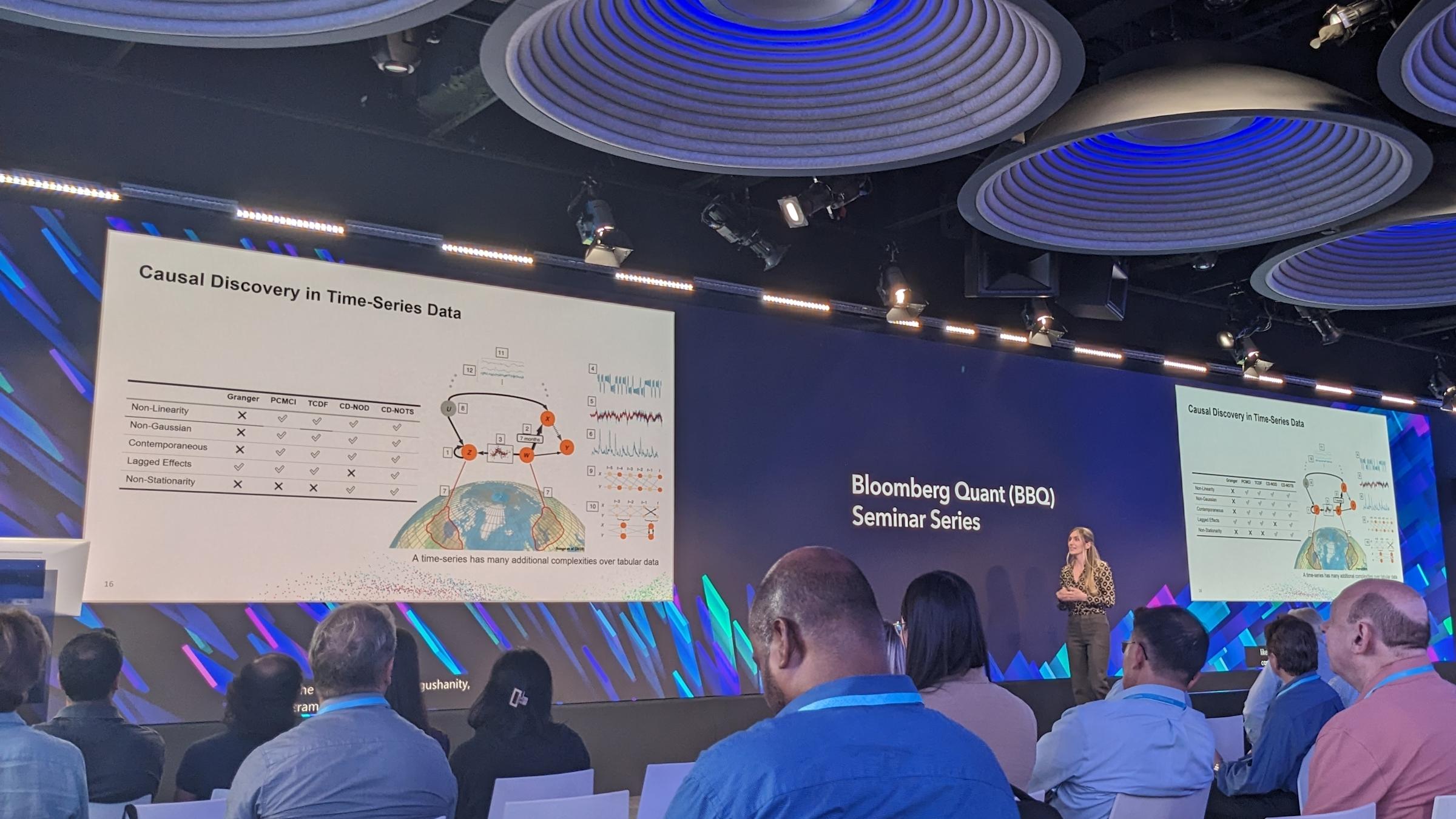

New research from Stevens School of Business Ph.D. candidate in Financial Engineering and Instructor Agathe Sadeghi, along with her co-authors Achintya Gopal and Mohammad Fesanghary, introduces a novel method for extracting the causal relations from time series data in their “Causal Discovery in Financial Markets: A Framework for Nonstationary Time-Series Data” paper.

The Gap

Causal study is a common practice in the social sciences and health care. For example, examining the effects of a public awareness campaign on reducing smoking by comparing data on smoking habits before and after the campaign or running a randomized controlled trial to determine the effectiveness of a new drug in reducing a specific medical condition. In these examples, the data sets are not in time series format.

“We mainly deal with time series data in the financial field,” explains Sadeghi. “The timestamp is very important.” Stock prices, exchange rates, interest rates, trading volumes and inflation rates are all time-series data that are recorded at specific intervals. Time series data have unique characteristics that have to be handled when dealing with them. However, existing causal discovery methods were not addressing them, creating a gap in the literature. “The existing literature in causal discovery wasn’t really handling the time concept very well. They weren’t addressing the different characteristics of these data types, such as nonstationarity, nonlinearity and contemporaneous and lagged effects,” she says.

Sadeghi and her co-authors wanted to work to fill that gap.

The Study

After identifying this important opportunity, Sadeghi and her co-authors began developing and testing an algorithm for causal discovery from nonstationary time series, referred to as the Constraint-Based Causal Discovery from Nonstationary Time Series (CD-NOTS), an extension of the CD-NOD algorithm (Huang et al., 2020) to handle time series data.

The team tested their algorithm on three financial case studies using real financial data, including macro data and company financials, to validate their work and measure the performance of their framework:

Analyzing the causal relationship between Fama-French factors and daily Apple returns from the beginning of 2000 to the end of 2022.

Monthly unemployment, Consumer Price Index (CPI) and Producer Price Index (PPI) data for the U.S., Japan, Canada, India, Italy, U.K., and France from 2000-2023.

Examining the causal relationship between the Price-to-Book ratio and returns of financial companies in the S&P 500 from 2010-2023.

“Causal discovery methods rely heavily on assumptions, hence testing for them should be a crucial part of any work,” she explained. The team categorized the assumptions into three categories and tested them:

Objective Assumptions: These are statistically testable assumptions, such as stationarity and linearity.

Algorithmic Assumptions: These assumptions refer to decisions in the causal discovery algorithm, such as hyperparameters, that can neither be directly evaluated nor justified purely by domain expertise. They did robustness tests for this set of assumptions.

Subjective Assumptions: These are assumptions that require domain expertise to evaluate.

The Results

Through their research, the team was able to determine causal connections among nonstationary time series data.

This research started when Sadeghi was interning in the Quant Research team of Bloomberg last Summer. Her work led to a paper she and her co-authors submitted to the ADIA Lab Award for Causal Research in Investment which was chosen as one of five finalists.

They had the chance to present their work this past June during the Bloomberg Quant (BBQ) Seminar Series, a testament to this growing field of research shared Sadeghi. “Causal research, I believe, is gaining more and more traction among the financial field and that paved the way for us to be the keynote [in the Seminar Series].” The audience’s reaction further confirmed her hypothesis. “Given that causal discovery is somewhat of a different topic from a traditional quant presentation, the audience was genuinely interested.”

The Implications

There are still more developments and larger investments that need to be made in this area of finance before causal methods are ready for industry use, but Sadeghi lays out some of the potential benefits once this work is brought to scale:

Identify the exposures on different stock returns to see if there is one driving factor on the return or if there is a group of factors acting together.

Use as a tool to search for statistically significant causal relations to determine if a trading strategy is reliable.