Ph. D. in Financial Engineering

From big banks to small hedge funds, companies in the financial space continue to aggressively seek professionals who can help the enterprise understand, assess and solve the challenges facing an industry that has been transformed entirely by new and emerging technology.

The interdisciplinary Ph.D. program in Financial Engineering at Stevens prepares students to become thoughtful researchers who can think about creative applications of technology and quantitative methods in building innovative solutions, designing new models, predicting risk and optimizing portfolios.

Graduates of the program go on to executive-level positions at companies such as Prudential and Goldman Sachs, where they apply engineering techniques in creating opportunities that drive the economy forward. The program's business orientation adds additional credibility for students eager to take on leadership roles in industry after graduating.

Stevens’ location — just a 10-minute ride from Wall Street — creates endless internship and placement opportunities, as well as the ability to attend conferences and work with industry on exciting research projects. And you’ll be supported and encouraged by faculty who are respected thought leaders eager to share their knowledge with doctoral students.

Who Should Apply

The Stevens Ph.D. in Financial Engineering is suitable for full-time students who are interested in pursuing careers in academia; however, most graduates go on to top-level positions in the financial industry, where they create new models or approaches to solve complex problems. Alumni of this program have gone on to executive-level positions at companies such as Goldman Sachs, JPMorgan Chase and Prudential.

Unlike many doctoral programs, the Ph.D. in Financial Engineering at the School of Business is specifically tailored to students interested in pursuing careers in industry upon graduation. While a Stevens doctoral degree in Financial Engineering is also suitable to those who wish to pursue academic careers, the unique bent of the courses in this program ensures students can compete for jobs at the highest levels in the finance industry, where their research will help companies create and refine new products and develop strategies to ensure competitive advantage in a quickly evolving industry.

While coursework is extremely challenging, students benefit from a supportive environment, working closely with both faculty mentors and fellow doctoral candidates. They also attend research colloquia that give fresh insight into the financial engineering challenges faced in industry and the tools and methods researchers are using to move the industry forward.

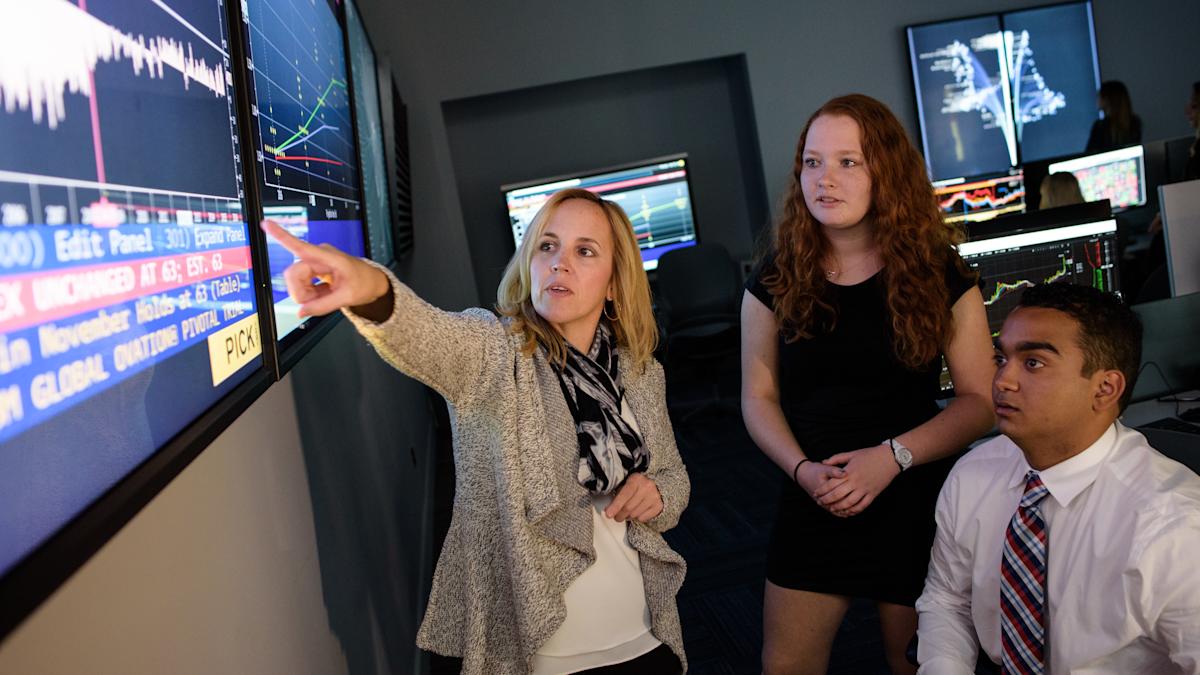

The other defining feature of the curriculum is its heavy emphasis on new technologies available through the Hanlon Financial Systems Center. Classes and lab courses go beyond basics in Bloomberg, OneTick, Thomson Reuters and more to ensure mastery of financial data sets and the ability to visualize real-time data to make better choices.

Required courses

Every doctoral student at Stevens completes PRV 961 Ph.D. Signature Course as part of their studies. In addition, Ph.D. students in the Financial Engineering program complete either MGT 719 Research Methods or SYS 710 Research Methodologies.

Area-specific courses

Working with their advisor, students choose from among the following courses to tailor their studies to their particular area of research interest. Additional courses may be substituted in with approval from the Ph.D. committee.

Quantitative methods

FE 641 Advanced Multivariate Statistics

FE 646 Optimization Models and Methods in Finance

MA 611 Probability

MA 612 Mathematical Statistics

MA 623 Stochastic Processes

MA 629 Convex Analysis and Optimization

MA 630 Numerical Models of Optimization

MA 653 Numerical Solutions of Partial Differential Equations

MA 655 Optimal Control Theory

MA 661 Dynamic Programming and Stochastic Optimal Control

MA 662 Stochastic Programming

FE 710 Applied Stochastic Differential Equations

FE 720 Volatility Surface: Risk and Models

Domain tools

FE 635 Financial Enterprise Risk Engineering

FE 655 Systemic Risk and Financial Regulation

FE 622 Simulation Methods in Comp. Finance and Economics

FE 670 Algorithmic Trading Strategies

FE 672 Modern Market Structure and HFT Strategies

CS 541 Artificial Intelligence

CS 559 Machine Learning: Fundamentals and Applications

CS 590 Algorithms

CS 600 Advanced Algorithm Design and Implementation

BIA 658 Social Network Analytics and Visualization

BIA 810 Cognitive Computing

Domain-specific research topics

Each course in the FE 801 series offers a deep dive into a particular area of financial engineering research. Students must complete one course from the below.

Advanced Topics in Portfolio Optimization

Advanced Topics in Market Microstructure and Algorithmic Trading

Advanced Topics in Financial Risk Modeling

Advanced Topics in Systemic Risk Modeling

Dissertation

Following completion of all written exams and coursework, students are required to write and defend a dissertation in a selected area of concentration. It is expected that doctoral dissertations will make significant contributions to the creation of knowledge and the development of theory and practice in a selected area.

Admission to the Ph.D. program is decided by the Ph.D. program committee at the School of Business, and is based on a review of the candidate’s scholastic record, professional accomplishments, and the fit between the student's research objectives and those of the school’s faculty. This allows the program to create invaluable opportunities for students to learn from, and work alongside, faculty who share their passion for research in algorithmic trading, mathematical finance, high-frequency trading, asset pricing, systemic risk, portfolio optimization, and financial analytics and innovation.

A list of Stevens admissions criteria can be found at Graduate Admissions. Some specialized requirements for admission to the doctoral program in Financial Engineering:

A bachelor's degree from an accredited institution, preferably in math, computer science, physics, engineering or finance.

For international students:

Candidates must achieve a TOEFL score of at least 90 or an IELTS score of at least 6.5 in each component.

Valid GMAT or GRE scores. Admission to School of Business programs is very competitive; excellent scores are required for candidates to be accepted.

A statement of purpose describing, in three pages, the applicant’s research interests and rationale, and general career objectives.

Current résumé or curriculum vitae.

Official transcripts for accredited schools of higher learning attended. Typically, a GPA of 3.0 (on a 4-point scale) or better at the bachelor’s level, and 3.5 or better at the master’s level, are required.

Three letters of recommendation.

Evidence of prior scholarly work. This work should be written solely by the applicant; published work under sole authorship will be highly valued.

Stevens taught me the foundations of data science, through the flexibility of carving out my own track in the Financial Engineering program. More importantly, my prior work experience in conjunction with my time at Stevens helped me bridge theory and practice, which is critical during these fast-paced transformational times.

Patrick Houlihan '16

Stevens taught me the foundations of data science, through the flexibility of carving out my own track in the Financial Engineering program. More importantly, my prior work experience in conjunction with my time at Stevens helped me bridge theory and practice, which is critical during these fast-paced transformational times.

Patrick Houlihan '16

Stevens taught me the foundations of data science, through the flexibility of carving out my own track in the Financial Engineering program. More importantly, my prior work experience in conjunction with my time at Stevens helped me bridge theory and practice, which is critical during these fast-paced transformational times.

Patrick Houlihan '16